Between computer network nodes, a blockchain is a shared distributed database or ledger. It functions as a digital database that electronically stores data. The most well-known use of this technology is preserving a secure and decentralized record of transactions in cryptocurrency systems like Bitcoin. By maintaining the accuracy and security of a data record, a digital ledger innovates by fostering confidence without the need for a trustworthy third party. To create the data chain known as the blockchain, each completed block is sealed and connected to the one before it. Blocks have fixed amounts of storage. Each piece of information that comes after the block that was just added is used to generate a new block, which is then added to the chain once the chain is full. It organizes data into chunks (blocks), contrary to databases, which typically arrange data into tables. When used decentralized, this data structure purposefully results in an irreversible chronology of data. A finished block is sealed forever and added to the timeline. Each block that is added to the chain receives a precise timestamp.

How a Blockchain operates

This digital ledger seeks to enable the unaltered sharing and recording of digital information. It serves as the basis for immutable ledgers, or records of transactions because they are unchangeable and cannot be added to, subtracted from, or destroyed. This is why distributed ledger technology and blockchains have similar names (DLT).

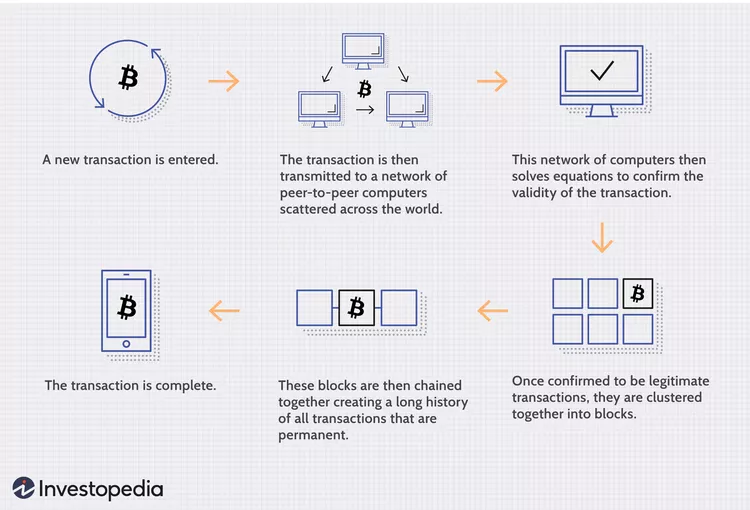

Process of a transaction

Decentralization of the blockchain

Think of a business that keeps a database of all the client account data on 10,000 machines in a server farm. This business owns the storage facility where all of these computers are kept, and it has complete authority over each one of them and the data they contain. If there was an electrical problem there, what would happen? What happens if the computer’s Internet connection is lost? What if it completely burns down? What would happen if a malicious person merely hit a key to wipe everything clean? The information is either flawed or insufficient.

It enables the distribution of the database’s data among several network nodes situated at diverse places. This preserves the accuracy of the data stored there while also enhancing redundancy; for instance, if a record is attempted to be modified at one database instance, the other nodes will not be tampered with, preventing a malicious actor from doing so. If one node interfered with Bitcoin’s transaction log, all other nodes would immediately cross-reference one another and identify the node with incorrect information. This procedure assists to come up with a clear chain of events. As a result, the data and history (such as cryptocurrency transaction history) are irreversible. A digital ledger may store a variety of data, including legal contracts, state identifications, or a company’s goods inventory.

Blockchains usage

As we all know, blocks on the blockchain of Bitcoin store information about financial transactions. On the blockchain, more than 10,000 other cryptocurrency systems are currently operational. It turns out, however, that doing so is a secure way to record data about different sorts of transactions. Just a few companies that have already embraced the technology include Walmart, Pfizer, AIG, Siemens, Unilever, and several more.

Blockchain advantages

Among the benefits of blockchain are the following:

The precision of the chain

On the blockchain network, transactions are approved by a vast computer network.. As a result, practically all human involvement in the verification process is eliminated, which reduces human error and ensures that the information is recorded accurately.

Reduced prices

Customers frequently pay a bank to validate a transaction, a notary to sign a document, or a minister to officiate a wedding. There is no longer a need for third-party verification, and with it, the associated expenditures.

Blockchain drawbacks

The following are some of blockchain’s drawbacks:

Cost of technology

Blockchain technology is not free, even though it can help consumers save money on transaction costs. For instance, the PoW mechanism used by the bitcoin network to validate transactions requires a lot of processing power.

Unlawful Activity

While privacy protection and hack prevention are provided by the blockchain network’s anonymity, it also makes it possible for illegal activities and commerce to take place there.

Take away

With various current real-world applications for the technology being deployed and investigated, blockchain is finally establishing itself, thanks in large part to bitcoin and cryptocurrencies. As an investor in the nation, everyone is talking about blockchain, which has the potential to eliminate intermediaries while boosting accuracy, efficiency, security, and cost-effectiveness in business and government operations.